Melt

Debt Payoff Planner

// the problem

The average Australian household carries $260,000 in debt. Credit cards, personal loans, car finance, HECS, and buy-now-pay-later balances add up fast. Most people know they should pay more than the minimum, but figuring out the optimal order, running the numbers, and tracking the plan is a task in itself.

Most debt payoff tools on the market are built for the US market (wrong currency, wrong assumptions), riddled with ads, or demand access to your bank accounts. For someone who just wants a clear plan on their phone without surrendering personal data, the options are thin.

// the solution

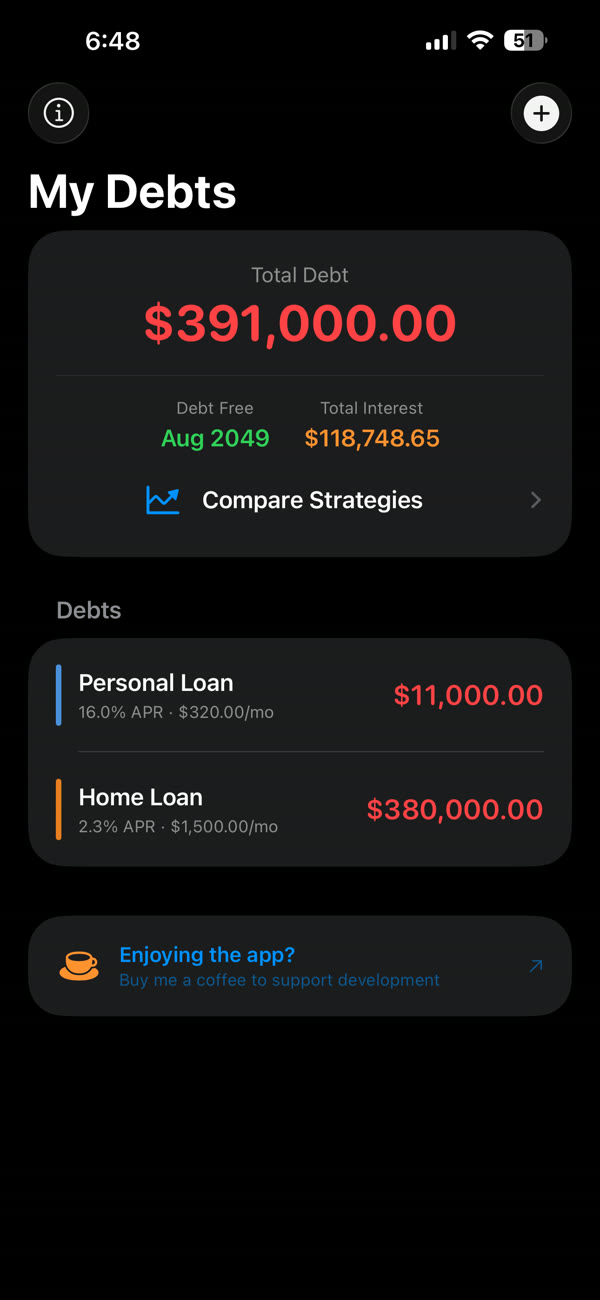

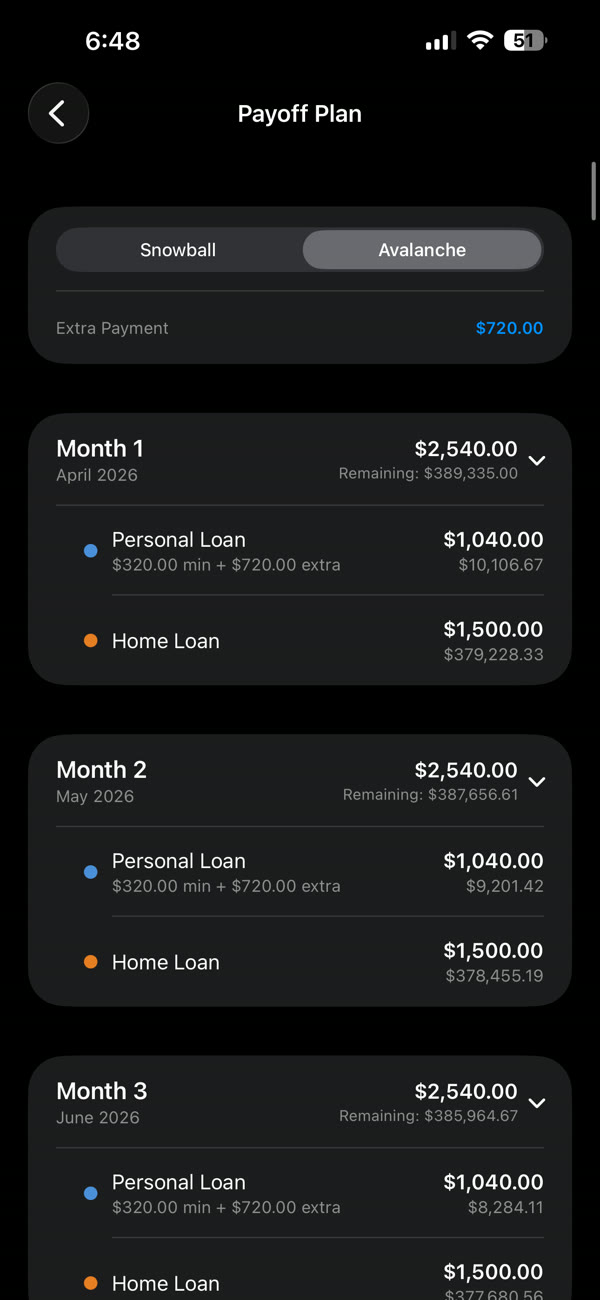

Melt is a free iOS debt payoff planner built for Australians. Enter your debts, pick a strategy (snowball or avalanche), set your extra payment amount, and Melt simulates the entire payoff journey. You see month-by-month plans, a balance chart showing your total debt declining over time, and exactly how much interest you save by making extra payments.

No accounts. No bank linking. No ads. Your data stays on your device. AUD currency formatting and Australian financial defaults from the start.

// snowball vs avalanche

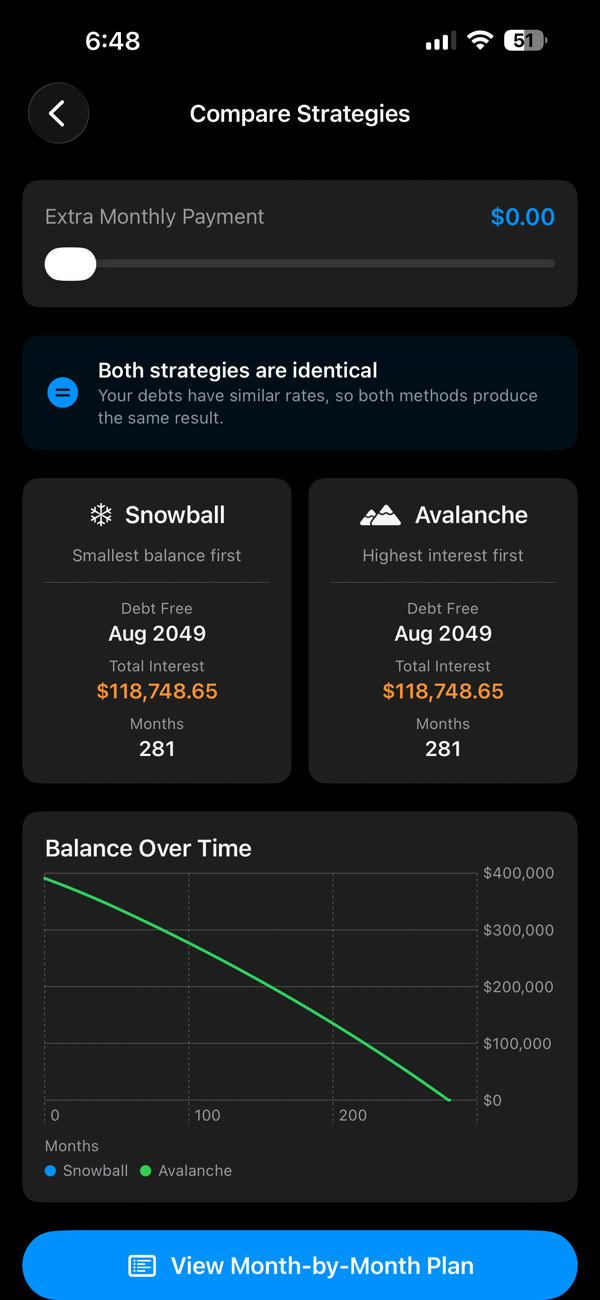

The snowball method orders your debts from smallest balance to largest. You throw all your extra money at the smallest debt first, pay it off, then roll that payment into the next one. The wins come fast, and the psychological momentum keeps you going. Mathematically it costs slightly more in interest, but behaviourally it works better for most people.

The avalanche method orders your debts from highest interest rate to lowest. You attack the most expensive debt first, saving the maximum amount of interest over the life of the plan. It takes longer to see the first debt cleared, but the total cost is lower.

Melt lets you compare both strategies side by side on the same debts, so you can see the real dollar difference and choose what fits your personality. Most users find the difference is smaller than they expected.

// who it's for

Melt is for anyone in Australia juggling multiple debts who wants a clear, private, no-strings plan. Apprentices managing car finance and a credit card. Graduates chipping away at HECS. Families with a mortgage, a personal loan, and buy-now-pay-later balances. If you have more than one debt and want to see the fastest way out, Melt does the maths.

// core features

// screenshots

// frequently asked questions

Is Melt really free?+

Yes. Melt is completely free with no in-app purchases, no ads, and no premium tier. Every feature is available from the moment you download it.

What is the snowball method?+

The snowball method is a debt payoff strategy where you order your debts from smallest balance to largest and pay off the smallest first. Once it is cleared, you roll that payment into the next debt. The quick wins build momentum and keep you motivated.

What is the avalanche method?+

The avalanche method orders your debts from highest interest rate to lowest and attacks the most expensive debt first. It minimises the total interest you pay over the life of the plan, saving you the most money overall.

Which is better, snowball or avalanche?+

It depends on your personality. Avalanche saves more money mathematically. Snowball gives you faster wins psychologically. Melt lets you compare both on your actual debts so you can see the real dollar difference and decide.

Does Melt need access to my bank account?+

No. Melt never connects to your bank, never asks for login credentials, and never sends data off your device. You enter your debts manually and everything stays on your phone.

Is Melt built for Australians?+

Yes. Melt uses AUD currency formatting by default and is designed for the Australian context (HECS, buy-now-pay-later, Australian interest rate conventions). It works for anyone, but it was built by an Australian for Australians.

Who built Melt?+

Melt was built by Jack Dempsey, a 4th-year electrical apprentice and indie developer based in Adelaide, South Australia, under the SEY Solutions brand.

// tech stack